Daliya’s financial diary shows a 27-year-old mother with multiple long-term health conditions living in South London. Before her children were born, she worked full time, but she later stopped working to care for her children, aged three and six.

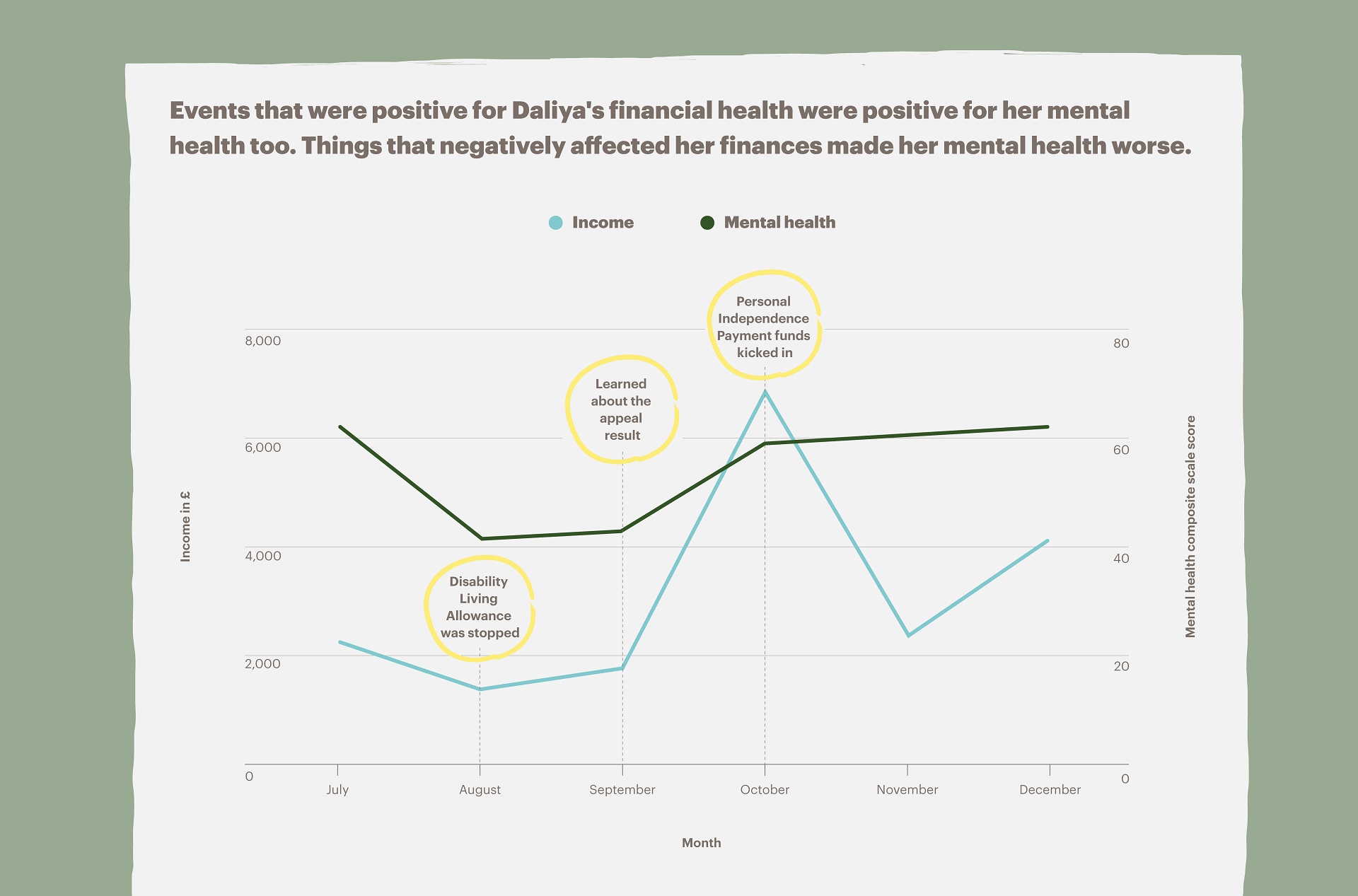

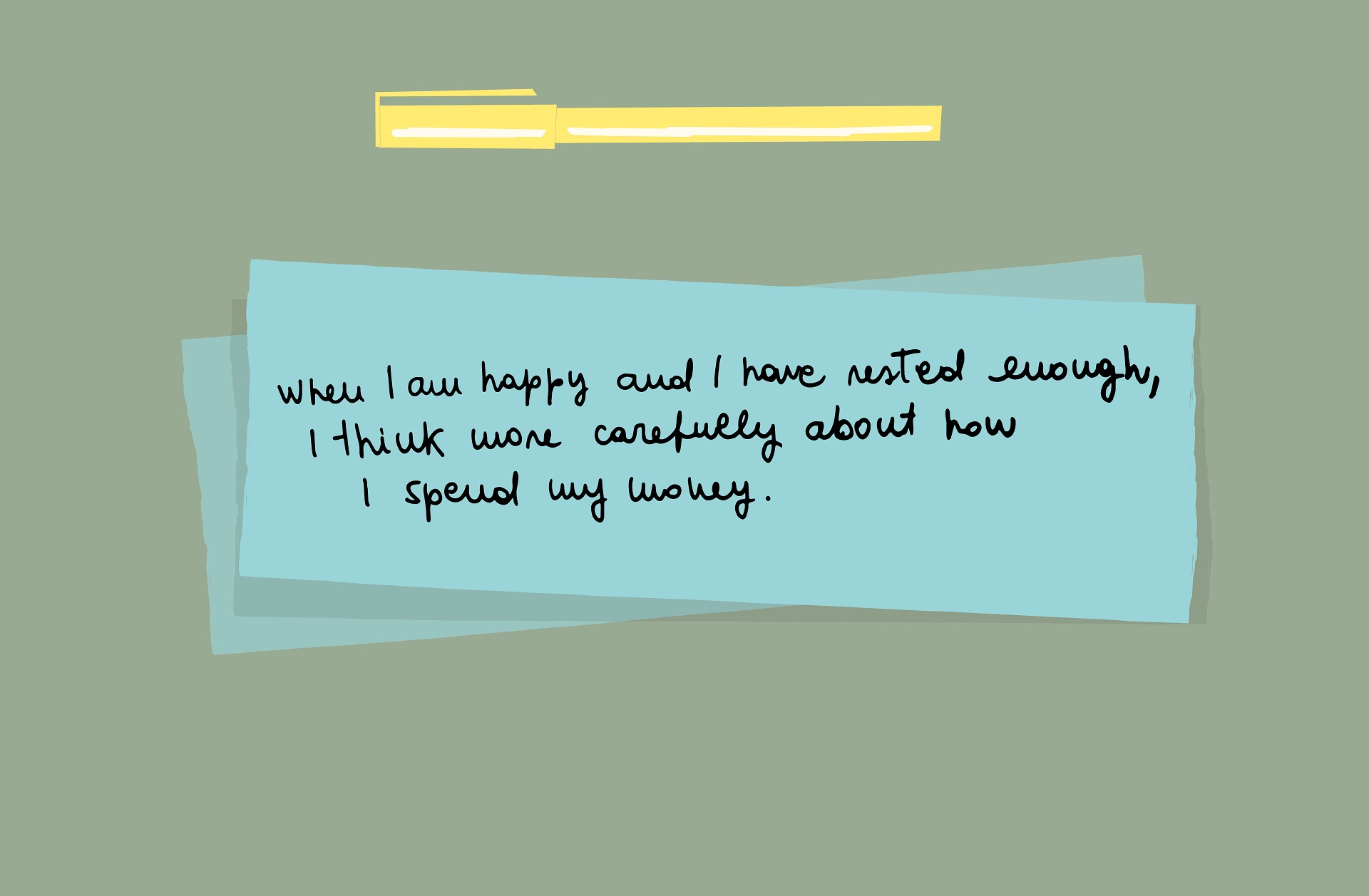

As a single mother, Daliya raises her kids alone and receives limited support from her children’s father. She is registered disabled and receiving means-tested benefits as well as disability and sickness benefits. Over the course of 2019 and 2020, however, Daliya experienced cuts and interruption to her benefits, making her unable to pay her bills at times. Unsurprisingly, this put a major stress on her mental health.

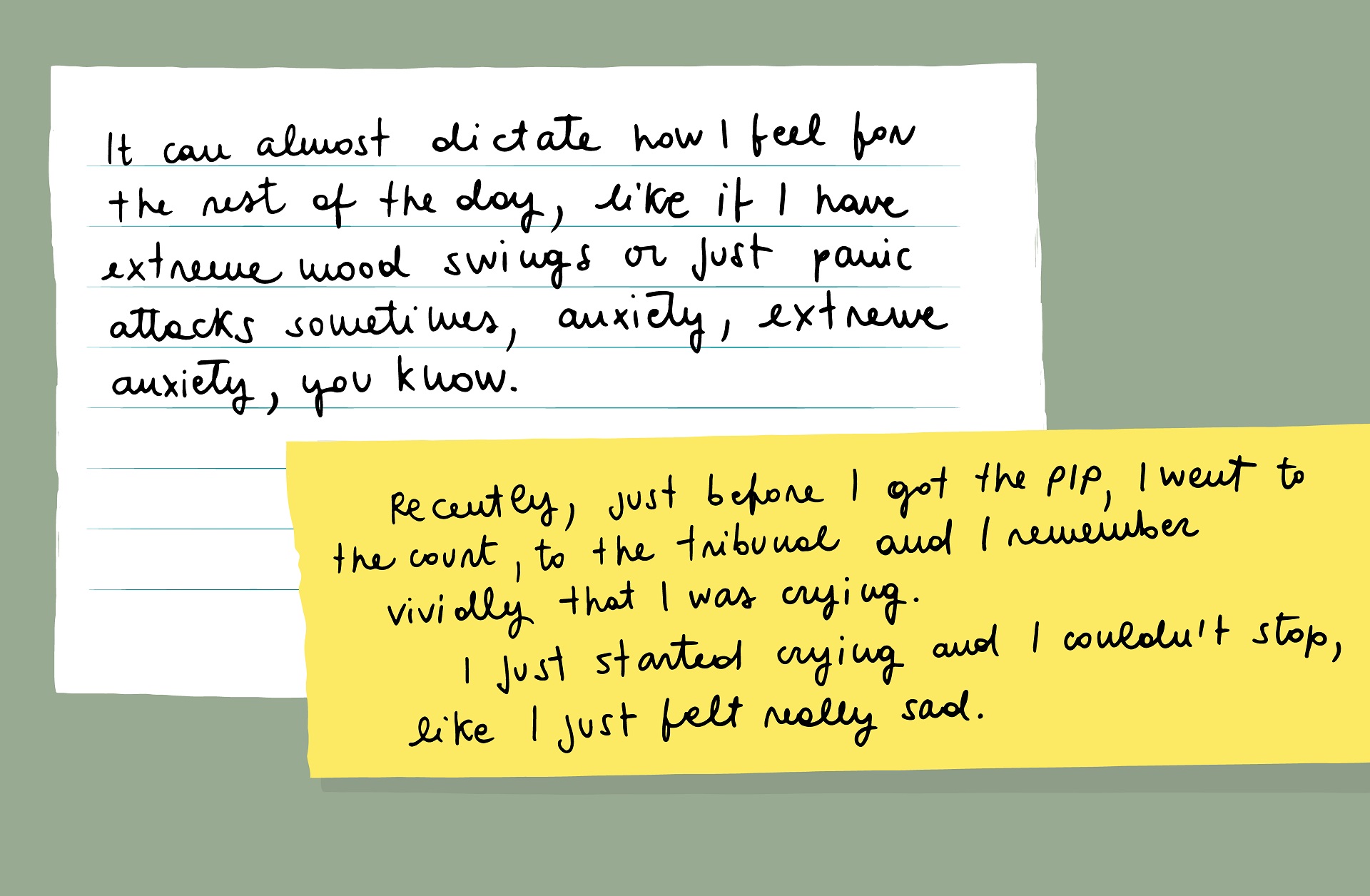

Daliya has lived with Nystagmus from birth; this is a vision condition in which the eyes make uncontrolled movements that often result in reduced vision and depth perception. On top of her vision condition, in 2016 she started to become unwell with anxiety, depression and bipolar disorders.

Three years later, in January 2019, she was diagnosed with prediabetes. These conditions severely challenge not only her sight, but also her daily activities.

Despite her daily challenges, Daliya actively looked for a job last Autumn while also trying to graduate from a part-time degree in Computing, IT and Mathematics. She paid for her education with a £3000 student loan. Since she had young children at home, she studied when they were at school or sleeping.

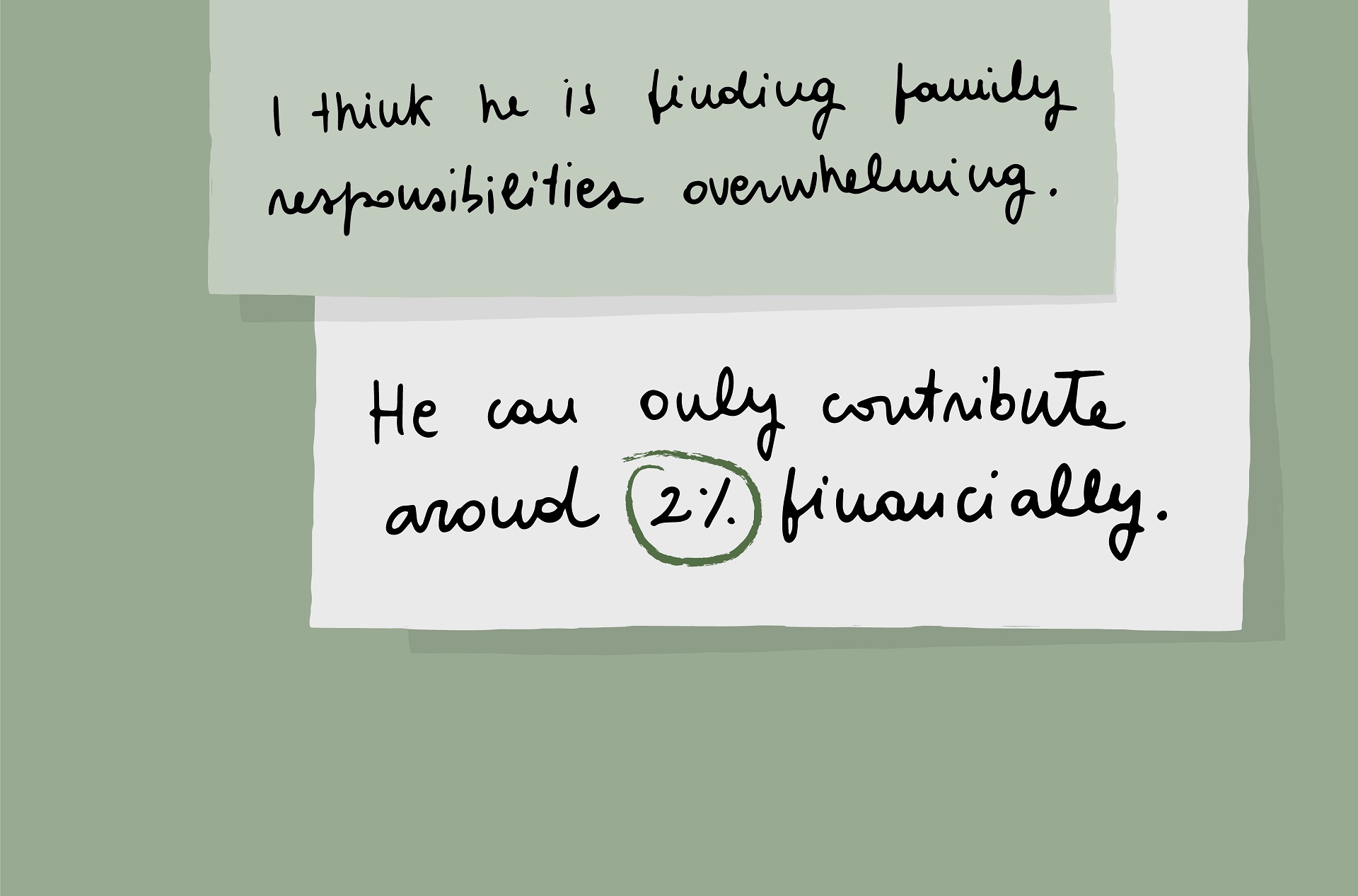

Ferdinand, the father of Daliya’s children, does not live with them, but does try to help the family by picking up their eldest son from school every day, supporting Daliya with showering her upper body, which she struggles to do by herself, and buying groceries.

Even though Ferdinand does the shopping, she pays for the groceries since Ferdinand does not have a stable job. Despite the assistance, Ferdinand’s help is not enough for Daliya. In an honest moment, she told us that money is a huge challenge, and she cannot count on anybody, not even him.