In 2019, her health conditions improved a little, so she started looking for a job again. Unfortunately, the family had no help with childcare and Luisa’s one-year-old only had 15 hours of free nursery per week, which limited the type of work Luisa was able to look for.

She felt constrained because she found it difficult to combine childcare responsibilities with low-pay work. In August 2019, Luisa’s family needed money, so she managed to find an informal cleaning job again.

It wasn’t a lot of hours nor much income, but she was afraid that if she got a more formal job, her family would lose entitlement to Universal Credit, which was the most reliable income she had at the time.

Without support to navigate the benefits system, Luisa made some employment decisions based on flawed assumptions. Unfortunately, she had to quit the cleaning job in September since her anxiety worsened again.

Luisa isn’t alone in this situation. Many people with multiple health conditions have limited ‘mental bandwidth’ to make financial decisions, which significantly increase their stress levels and anxiety.

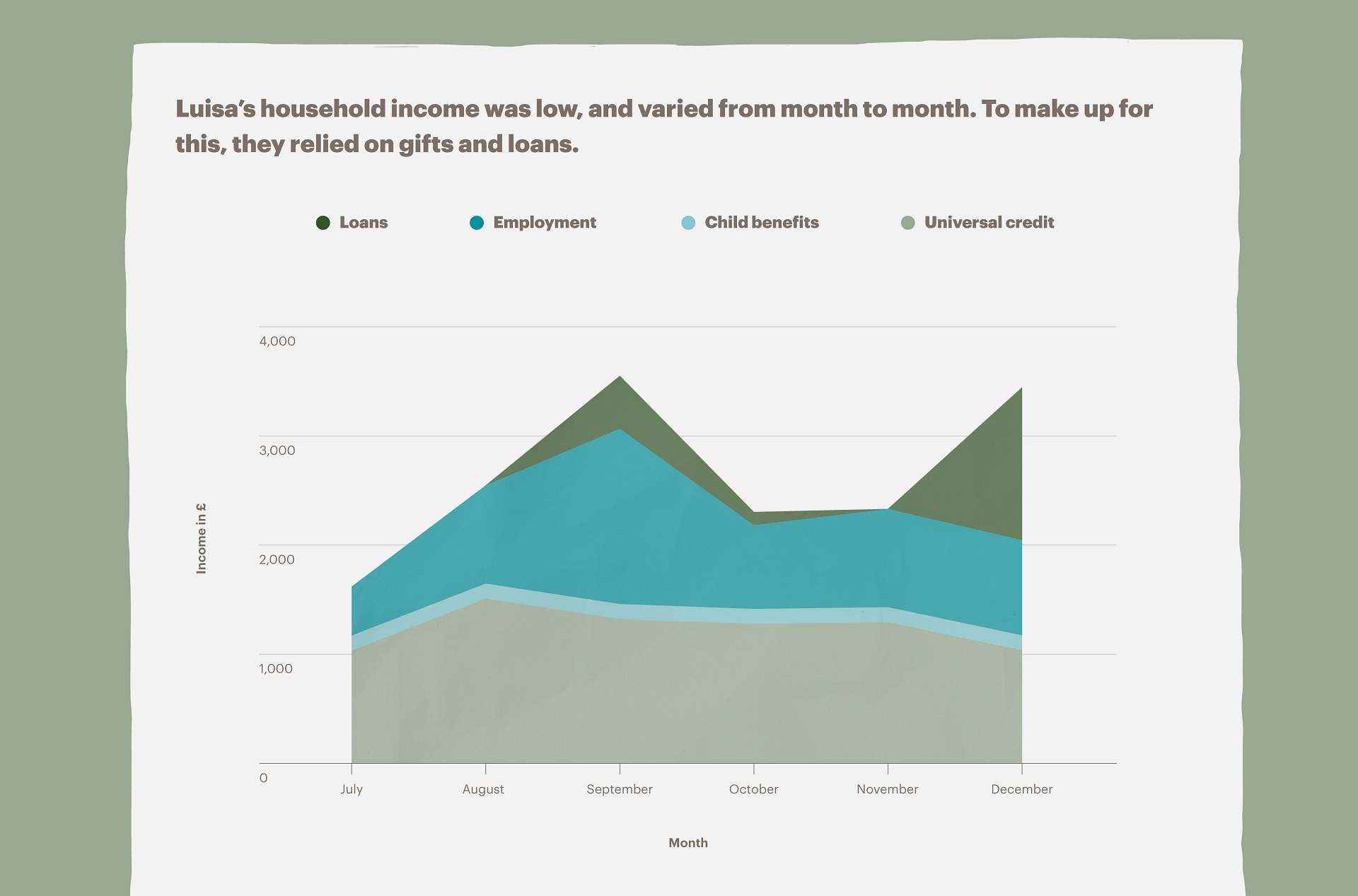

Luisa’s household income was not only low, but also varied from month to month (see graph below). Her husband Tony worked on a zero-hour contract, and his salary did not always cover essential expenses.

When they were strapped for cash, they mostly relied on loans and gifts from Tony’s mum and Luisa’s aunty. Sometimes, however, their family were not in a position to help, and Luisa and Tony asked others for loans, including Luisa’s boss.

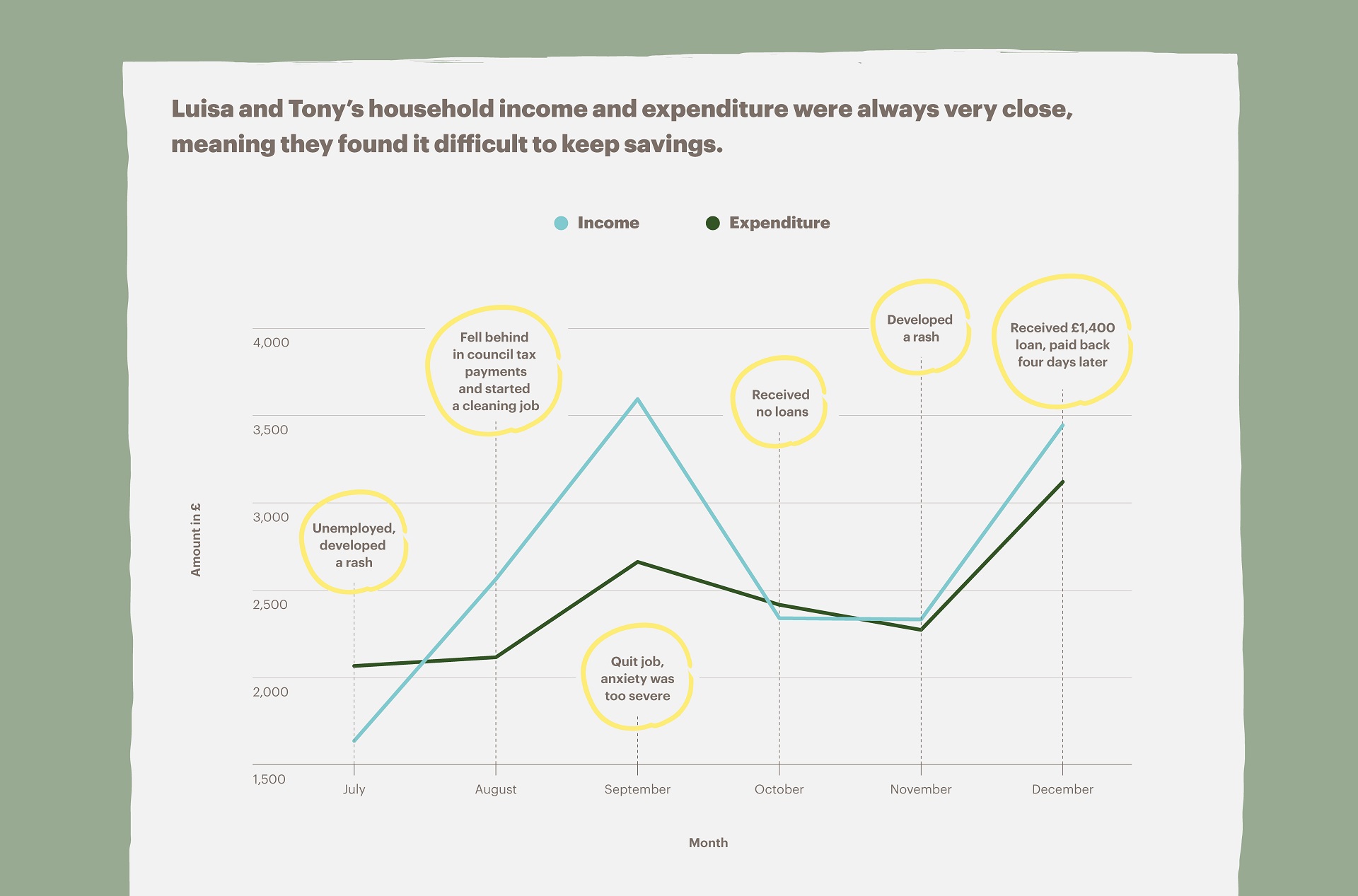

Fig. 6